No one was prepared for what the world has experienced over the past 18+ months. Globally, the pandemic is far from over and continues to influence much of our everyday lives. Given its impact, the ripple effects, many of which are economic and financial in nature, will be felt for years to come.

Even after living with COVID-19 for almost two years, the widespread disruption continues to alter Australian consumers’ financial situations, which has resulted in seismic shifts in spending behaviors across the country. In addition to what consumers are buying and where they are spending their money, consumers are also approaching their payment preferences differently than they did pre-pandemic.

Given financial strain and concerns about hefty interest rates amid economic uncertainty, more than 1 million Australians have cancelled their credits over the past year. But they didn’t do so without having an appealing alternative to turn to. Notably, the allure of digital payment systems offering interest-free payment installments has sparked interest and adoption at a time when many consumers are focused on frugality and looking for more practical offerings from their financial service providers.

Buy now, pay later services aren’t new financial options for consumers, but their appeal among Australians has been on the rise since entering the market in 2015. That rise then increased notably when the effects of the pandemic set in, bolstered by the flexibility and convenience of interest-free payment plan options—a dramatically different alternative to traditional credit cards.

On the ground, adoption over the last year has risen quickly, as the Reserve Bank of Australia reported in March of 2020 that buy now, pay later transactional values had risen by 55%. In its national survey, Australian research consultancy DBM Atlas reported in June 2021 that approximately 14% of Australian adults had made a purchase using a buy now, pay later service in the past four weeks—up from 11% a year earlier.

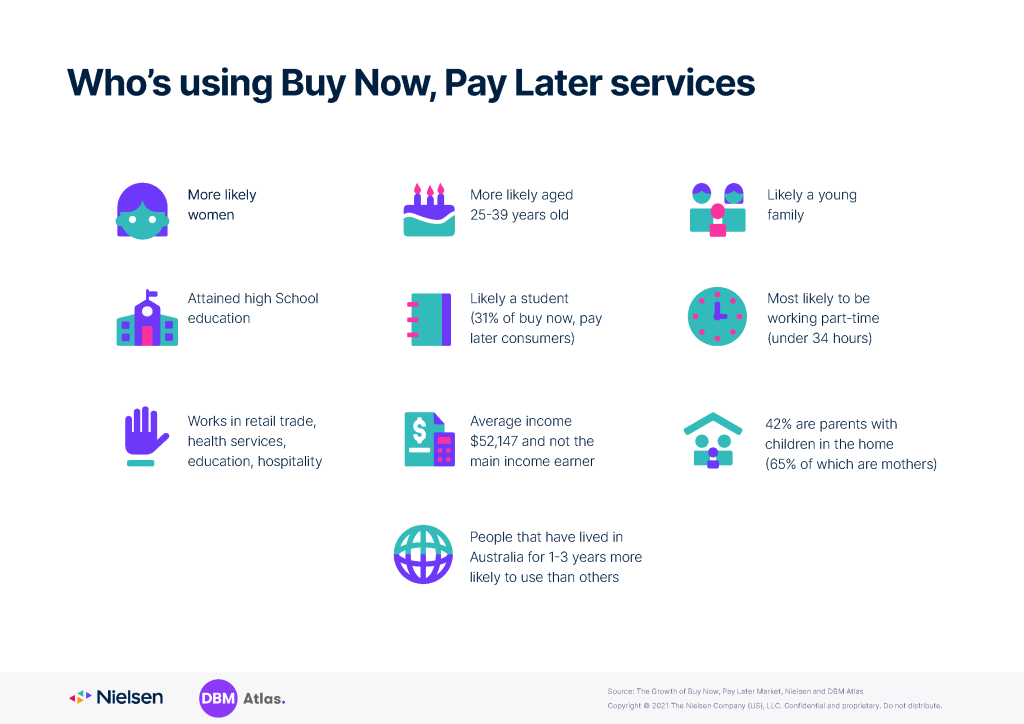

While adults of all ages are using buy now, pay later services, younger consumers are driving much of the growth—and will continue to do so into the future. Nielsen research shows that almost two-thirds of Australians who have used buy now, pay later payment methods are aged 18-44.

An array of sectors have benefitted from the increased adoption of these payment services, but the upside for clothing, fashion, mobile phone and tablet retailers has been particularly bright, especially when you consider the effects of the pandemic on non-essential shopping trends. Research from Nielsen and DBM Atlas has found that these payment services have opened the door to a new generation of consumers, while improving sales potential for both online and in-store across a wider buyer base. In some retail categories, the adoption has led to bigger basket sizes and has even incentivised customers to spend more than they initially intended.

With connectivity and online engagement well above norms during much of 2020, Nielsen expects that the shift in spending patterns will remain as consumers begin to resume some—or all—of their pre-pandemic activities.

Additional insight into the growth of buy now, pay later services is available in a new joint Nielsen-DBM Atlas report. Additional information about the report and purchase options can be found here.

Methodology

NIELSEN RESEARCH & DBM ATLAS METHODOLOGY

Nielsen has integrated award winning DBM Atlas – Australia’s largest research program dedicated to financial services with Nielsen’s Consumer & Media View (CMV).

DBM Atlas + Media Profiler provides a segmentation and profiling dataset specifically developed for the banking, insurance and wealth management categories.

DBM Atlas + Media Profiler offers thousands of attitudinal, media and behavioural variables for in-depth consumer understanding – including how to best reach and engage key audiences.

- 93,000 respondents

- CMV: 100% Online; In field 48 weeks of the year

- DBM Atlas: RDD fixed line / mobile and online panel; Online completion continuous, daily

- 14+ National

- Results weighted using ABS to accurately reflect the Australian population (000s)